Personalized Loan Solutions

Cash-Out Refi

Construction

Acquisitions

Bridge Loans

Hard Money

Distress + Time Sensitive

1 to 30 Year Terms

Prime Resource Capital LLC is solely dedicated to lending for investment and business purposes. Please note that Prime Resource Capital LLC does not provide loans for primary residences or for personal purposes.

At Prime Resource Capital, our mission is to provide customized financing solutions to help real estate investors achieve their goals.

We strive to be a trusted partner to our clients, offering expert guidance, responsive service,

and flexible loan products that meet their specific needs.

Our goal is to help our clients grow their real estate portfolios and achieve long-term financial success, while maintaining the highest standards of integrity and professionalism in all of our business practices.

Asset Classes

Prime Resource Capital specializes in providing financing solutions for a variety of investment real estate asset classes.

1-4 Family Residential

Single-family homes, townhouses, and condos.

Multi-Family Residential

Apartment buildings and other multi-unit residential properties.

Commercial

Office buildings, hotels, motels, retail centers, and warehouses.

Mixed-Use

Retail, office or commercial with residential.

Industrial

Factories, warehouses, and distribution centers.

Land

Entitled undeveloped or partially developed urban land.

Solutions

Hard Money and Private Money Loans

Our hard money loans offer flexible financing options for investors who may not meet traditional lending requirements. These loans are ideal for fix-and-flip investors and other short-term real estate investments.

Stated Income Loans

Our stated income loans are designed for investors who may have difficulty providing traditional income documentation. With no income verification, these loans offer a streamlined financing solution for investors seeking to acquire investment properties.

Bridge Loans

Our bridge loans provide short-term financing solutions that can help investors acquire or rehabilitate properties quickly. These loans are ideal for investors who need to move quickly to capitalize on a real estate opportunity.

Commercial Real Estate Loans

Our commercial real estate loans offer financing solutions for investors seeking to acquire or refinance commercial properties, such as office buildings, retail centers, and multi-family buildings.

Institutional Real Estate Debt and Equity Products (over $25mm)

In addition to our direct lending services, we also offer a range of real estate debt and equity products to our larger sponsor clients, including preferred equity, mezzanine debt, bridge loans, senior debt, and other debt and equity investments. Our experienced team of advisors works closely with our institutional clients to identify opportunities that deliver attractive returns while satisfying the needs of our sponsors.

Our middle market capital providers include private equity firms, hedge funds, real estate investment trusts (REITs), institutional investors, life insurance companies and other non-bank lenders.

At Prime Resource Capital, our focus is on being a solution provider to all real estate investors. We offer customized loan options and a wide range of real estate debt and equity products that help investors achieve their investment goals while delivering value to our investors.

Our experienced team of advisors works closely with clients to match our products to their specific needs, providing customized financing solutions and real estate debt and equity products that help them achieve their investment goals.

Our real estate debt products are designed to provide investors with the capital they need to achieve their investment goals, whether that's acquiring a new property, refinancing an existing investment, or executing a successful fix-and-flip project.

We're committed to providing our clients with exceptional service and value, and we're dedicated to helping you achieve your real estate investment objectives.

Contact us today to learn more about our real estate debt products and how we can help you succeed in the real estate market.

Client Feedback

"My experience was fantastic very responsive plenty of orientation to get the deal done. Everything happened on time the customer service was top-notch.

They took a complicated situation and made it easy and I was approved in no time I would highly recommend. Prime was fantastic"

-Jose T. Esq

"Best experience... first time I didn’t know I was going to qualify but Prime came through.

Prime actually gave me my breakthrough and was able to qualify for 8 more properties.

Stick to it all timing be patient I have nothing to say besides Prime was great, customer service was quality, great return timing, and they would always call first.

I would definitely recommend other customers to work with Prime Resource Capital."

-Durvijai P.

"needed a 1031 exchange done...within 21 days we were able to close a full document loan... he listened to the challenges... and most importantly, he provided advice as to to position myself for a success exit... I would reach out to them right away "

- Jerome H.

"They truly work with you to get the help you need. They go above and beyond to help. I highly recommend this company and it was a pleasure doing business with them, keep up the good work helping others."

-Chandrawatie R

"I googled for hard money loans, and ran into Prime Resource Capital and it was the Salvation I needed!

I would definitely recommend Prime's service to other property owners and seekers."

-Diana R.

"Prime Resource was so helpful in getting us the funding we needed to purchase another fix and flip.

Thank you for the fast and smooth transaction."

– K.C. Dallas, TX

"We had gone to many other hard money lenders and found that Prime Resource Capital offered the best services and lowest rates.

The trust factor played a big part in decision to go with Prime and we’re glad we did."

– E.L. Phila, PA

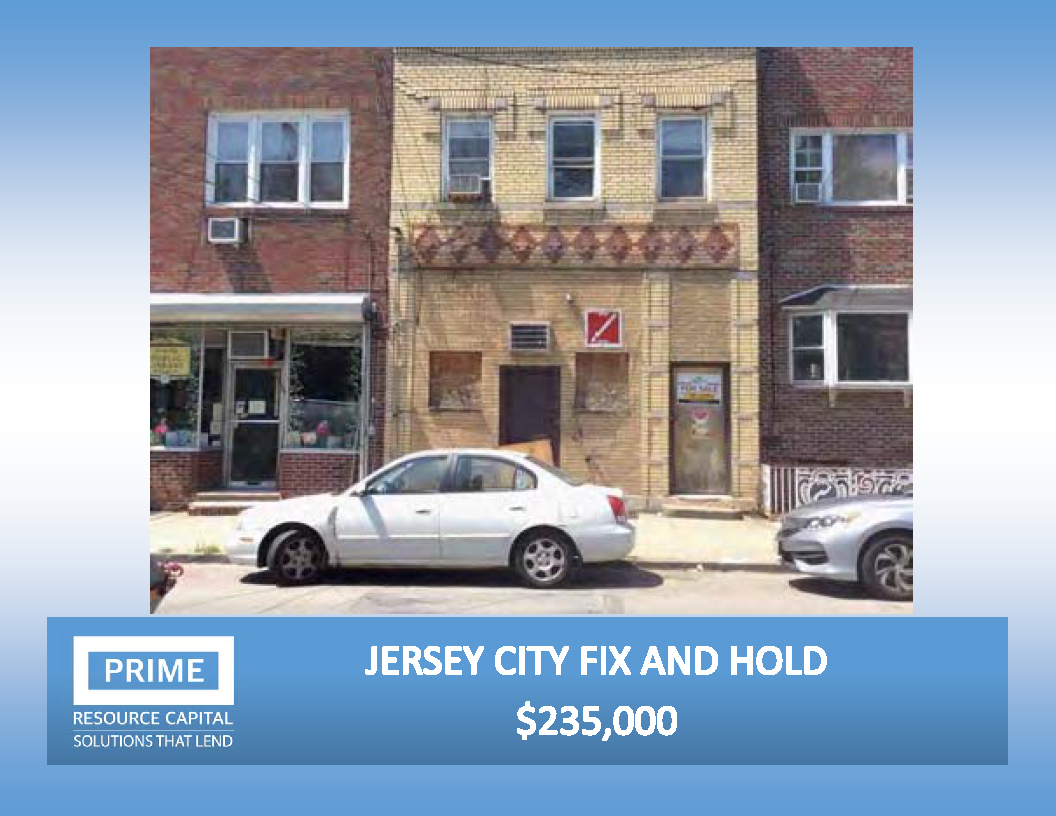

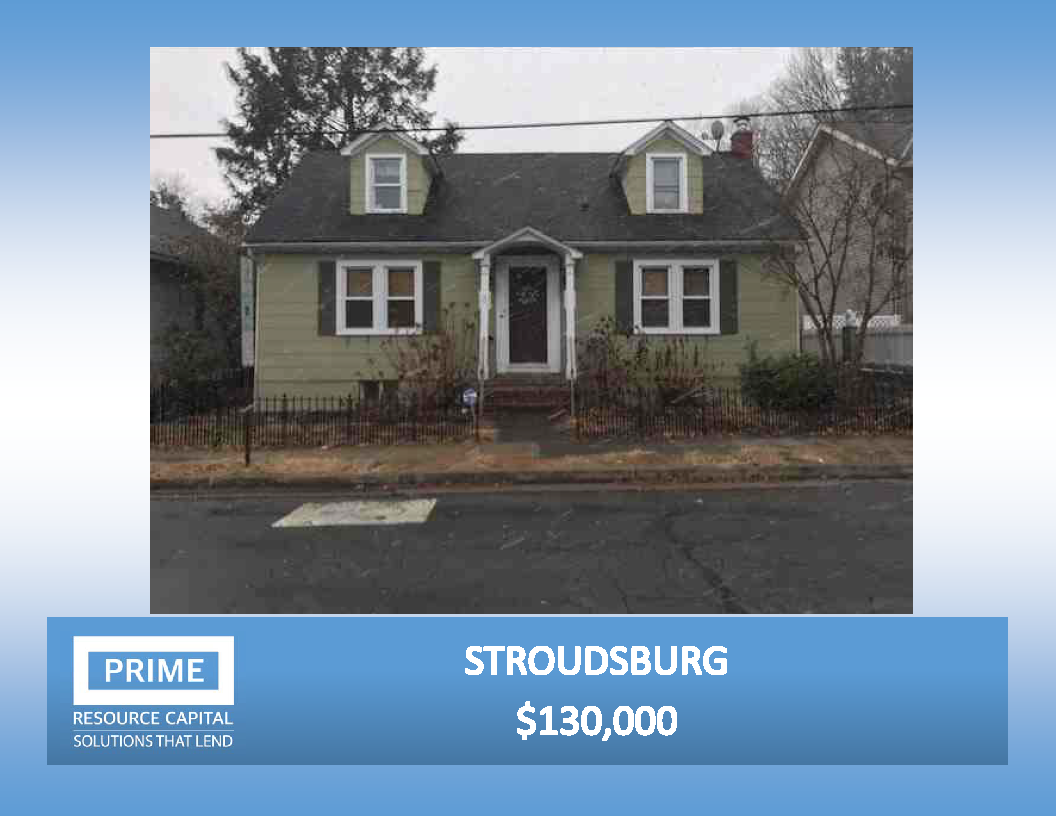

Notable Deals

$10MM+ Capital Solutions

Whether you're a seasoned real estate developer or an ambitious entrepreneur entering the field, securing the right funding for your project is crucial.

At Prime, we understand this, offering a wide range of loan products designed to meet the diverse needs of real estate professionals across the Capital Stack.

Senior Debt

This type of loan is the most secure, having first claim on the income and assets of the property. Prime Resource Capital offers competitive rates and flexible terms for senior debt loans, making them a reliable choice for your primary financing needs.

Mezzanine Debt

This is a form of subordinate financing that is typically used to fill the gap between senior debt and equity. With a higher risk profile, mezzanine debt comes with a higher interest rate but can be an effective way to boost your project's potential returns. Prime Resource Capital can provide mezzanine financing that aligns with your project's risk and return profile.

Preferred Equity

Preferred equity is another form of subordinate financing that provides a fixed rate of return before common equity holders receive any profits. It's a versatile form of capital that can be structured to fit a variety of financing needs. Prime Resource Capital offers preferred equity solutions that are tailored to your project's specific needs.

Joint Venture Equity

For projects requiring substantial capital or unique expertise, a joint venture can be an excellent solution. Prime Resource Capital can provide joint venture equity, partnering with you to share in the risks and rewards of your project.

Bridge Loans

These short-term loans are designed to cover an immediate expense while securing long-term financing. Prime Resource Capital's bridge loans can provide the quick, flexible funding you need to keep your project moving forward.

Construction Loans

If you're planning a new development, Prime Resource Capital's construction loans can provide the necessary funds to get your project off the ground. These loans are structured to disburse funds as construction milestones are met, providing a steady cash flow throughout the building process.

Permanent Loans

Once your project is completed, you may want to secure long-term financing with a lower interest rate. Prime Resource Capital's permanent loans can provide the stability and predictability you need for your completed project.

Prime Resource Capital understands that each real estate project is unique, and they're committed to providing personalized, flexible financing solutions that fit your specific needs.

Reach out today to discuss how they can help secure your next project.

Ready to achieve your goals?

Follow these three simple steps to get started:

Step 1

Connect with our team and receive a customized quote that fits your unique needs.

Step 2

Discover our wide range of financing options and choose the one that's right for you.

Step 3

Get funded quickly and start making progress toward your success story.

Don't wait – let us help you reach your full potential today.

At Prime Resource Capital, we understand that time is of the essence when it comes to real estate investing.

That's why we offer fast, flexible financing solutions that can help you achieve your goals on your timeline.

Contact us today to get started.

...Yes!

There Really Is a Difference if You use the Wrong Lender.

Experience: Prime Resource Capital's management team has over 30 years of experience in real estate lending, providing expert knowledge and guidance to help you navigate complex transactions.

Personalized Service: Prime Resource Capital takes a personalized approach to lending, taking the time to understand each borrower's unique situation and offering tailored solutions to meet their needs. This level of personalized service sets them apart from larger, more impersonal lenders.

Speed and Flexibility: Prime Resource Capital is able to move quickly and provide flexible lending solutions, which is particularly important for real estate investors who need to move quickly to secure investment opportunities.

Affordable Financing: Prime Resource Capital provides affordable financing solutions with competitive interest rates and fees, helping you to achieve your real estate investment goals while staying within your budget.

Trusted Reputation: Prime Resource Capital has earned a trusted reputation in the industry, with a high level of customer satisfaction and an A+ rating from the Better Business Bureau. You can be confident that you are working with a reliable and trustworthy lender who has your best interests in mind.

Frequently Asked Questions

Can I use cross-collateral for my private loan?

Yes, cross-collateral investment properties may be used to secure a private loan.

Do you offer loans for Primary Residences?

Unfortunately, no. We only lend funds based on real estate assets that are not the borrowers primary residence.

Can I get a private loan for a distressed or auction property?

Yes, we offer private loans for distressed and auction properties.

Please call for more information.

Do you require tax returns?

Tax returns are not required for stated income loans, private loans nor hard money loans.

Do you offer loan pre-approvals letters for purchases?

Yes, we offer conditional pre-approvals.

Please provide the subject address, purchase price and signed credit release, current bank statements showing the deposit monies, and scope of work and value after repair (if needed).

Call 888-772-7720

What is the typical turnaround time for loan approvals?

Depends on the loan program you will qualify for. We've closed loans in as fast as 3 business days.

How long can I borrow for?

Loans typically have maturities of 1 year to 30 years.

Do you require a minimum credit score for loan approvals?

It depends on the type of loan you are seeking. We have worked with no credit to 850 credit.

Call us to discuss. 888-772-7720

Do you charge any prepayment penalties?

Prepayment penalties will vary from loan program to program. Call for details.

What is the typical interest rate for your loan products?

Interest rates fluctuate daily for all of our programs. Call for the best available rates.

Disclaimer: Prime Resource Capital LLC is a direct lender that provides financing solutions to businesses and real estate investors. We do not offer loans for personal, non-business related purposes. All loans are subject to our underwriting criteria, which may include factors such as creditworthiness, collateral value, and borrower financial capacity. Loans made or arranged by Prime Resource Capital LLC are for business and investment purposes only and not for personal, family, or household use. It's important to note that while we strive to provide the most accurate and up-to-date information, the information contained in our marketing materials, including our website and other publications, should not be considered legal, financial, or investment advice. Additionally, Prime Resource Capital LLC is not affiliated with any government agency, and we do not guarantee the accuracy, completeness, or timeliness of any information presented on our website or other marketing materials. If you have any questions or concerns about our services or loan products, please don't hesitate to contact us. Our team of experienced lending professionals is dedicated to providing exceptional service and support to help you achieve your financial goals.